Understanding sequence of returns risk

Retirement planning should start at the onset of your professional career. Like many things in finance, the earlier, the better. Many residents and fellows can save into a retirement plan and receive matching contributions even during their training. Over the next 30-plus years as a medical provider, your investment returns will play a role in your preparedness for retirement, but returns are not the only important variable. You’ll also have to manage your lifestyle expenses, retirement savings, and many other aspects of creating a sound retirement plan.

Understanding sequence of returns risk

Many have become familiar with a risk over the last 15 years called the sequence of returns risk (SORR). That is, the risk a late-career professional or early retiree will experience negative investment returns. The risk becomes more prominent later in your career since it gives you less time to make up for losses that may also be compounded by account distributions.

Many people have heard horror stories of friends and family members trying to retire during the 2008 financial crisis. These horror stories exist primarily due to the sequence of returns risk.

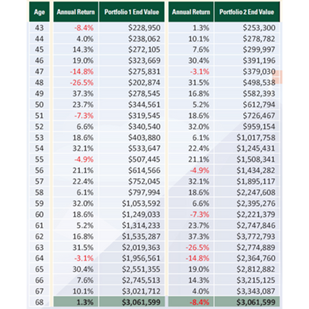

Timing matters

Take two mid-career investors, in which both investors have a portfolio size of $250,000 at age 43. Over the course of the next 25 years, each investor received the same returns but in the opposite order. Here are their investment results (utilizing the S&P 500 Index as their investment):

Since both investors were in the accumulation phase of their retirement planning, both ended with the exact same account value despite the order in which their returns were received.

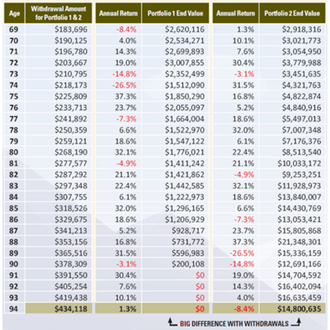

Now, take those same two investors. Both are now at retirement and require annual distributions equal to 6 percent of their portfolio in the first year, with 3.5 percent increases annually thereafter. Both investors start with a portfolio of $3,061,599.

As you can see, the order in which the investors receive their investment returns during their Distribution Phase of retirement planning becomes much more critical during periods of withdrawals due to the sequence of returns risk. In the example above, the first investor runs out of money, and the second investor has a portfolio valued at $14,800,635, despite having withdrawn more than $7,500,000.

This sequence of returns risk is real and can have a long-lasting emotional and financial impact on some of the best years of your life.

Here are three action items you may utilize to mitigate the sequence of returns risk in retirement.

1. Review your portfolio allocation. As you approach retirement, the risk within your portfolio or often the exposure to stocks isn’t required to be the same as at the onset of your career. Therefore, as you near your retirement date, reviewing your portfolio allocation becomes much more critical to determine if you are aligned appropriately with your goals. This phenomenon occurs automatically in many employer-sponsored retirement plans such as 401(k), 403(b), 457(b), or 401(a) plans if you are utilizing a Target Date Fund. For example, a target date fund allocation for someone 35 years away from retirement often has 90 percent stock exposure. In contrast, someone within five years of retirement has approximately 55 percent exposure to stocks. In addition, not all investments or mutual funds adjust their exposures over time. Therefore, you must review and fully understand how your accounts are allocated.

2. Understand your comfort level for volatility during retirement. In 1978, Congress passed the Revenue Act of 1978, allowing employees to defer their income to a Section 401(k) plan. Before this, most employers offered pension plans. Today, and for the last many years, this means the responsibility for retirement income planning has shifted from an employer’s responsibility to an employee’s responsibility. Therefore, it’s important to determine whether you are comfortable with the potential for a variable retirement income plan (taking distributions from investment accounts as needed) or if you’d prefer more stability in your income planning during retirement. Although pension plans are nearly extinct, there are other solutions available to help retirees receive stable income throughout retirement.

3. Keep adequate cash reserves to avoid withdrawals in poor market years. Another way to reduce your sequence of returns risk would be to utilize a bucket retirement income planning strategy. To maintain adequate cash reserves, supplement one to three full years of your needed retirement income. Of course, this does create other risks but can help prevent the sequence of returns risk by using cash reserves during volatile market years and then replenishing your cash reserves once your investments have recovered.

Contemplating retirement?

It’s impossible to predict the future or foretell the market environment when you are ready to retire. Yet, timing can profoundly affect your ability to sustain your income if you plan to withdraw your accumulated assets systematically.

Jordan Bilodeau is a certified financial planner.

Disclosure: The illustrations above are hypothetical and for illustrative purposes only and are not representative of any product. The Standard & Poor’s 500 Composite Index (S&P 500) is an unmanaged index of 500 common stocks generally considered representative of the U.S. stock market. Indexes do not consider the fees and expenses associated with investing and individuals.

Securities, investment advisory, and financial planning services are offered through qualified Registered Representatives of MML Investors Services, LLC. Member SIPC. Supervisory office: 4350 Congress Street, Suite 300, Charlotte, NC 28209, (704) 557-9600. Spaugh Dameron Tenny is not a subsidiary or affiliate of MML Investors Services, LLC or its affiliated companies. CRN202601-3761265.